Quarterly Investment Letter

3rd Quarter 2018

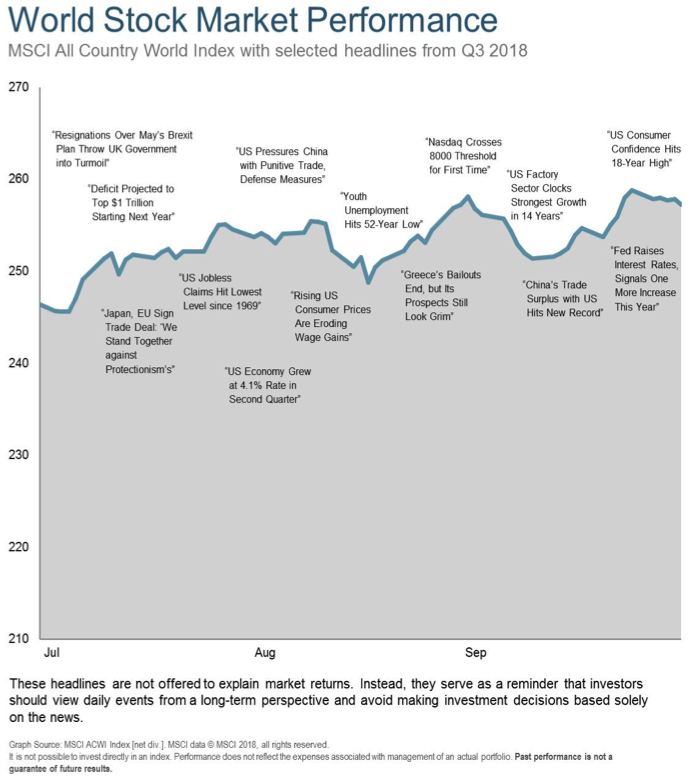

Global equity markets overall closed 2018’s third quarter with an advance. However, trade relations continued to worry many investors, in particular surrounding China. Economic troubles in Turkey and Argentina also weighed on certain markets. Some observers took cheer in promising trade negotiations, such as the European Union and Japan agreeing to create one of the world’s biggest liberalized trade zones. Additionally, negotiations that continued through the last day of the quarter added Canada to a US-Mexico trade deal initially announced in late August. The MSCI All Country World Index generated a 4.4% total return for the quarter.1 Developed-market stocks, as measured by MSCI indexes, recorded an overall rise ahead of the global index, while emerging-markets retreated.1

The US stock market’s performance increasingly separated itself from the rest of its developed-market peers. Robust corporate earnings, high business and consumer confidence, multi-decade low unemployment and strength in other economic indicators all supported US equities.2 The nation’s gross domestic product (GDP) expanded at a 4.2% annualized growth rate in the second quarter.3

European equity markets as a group were almost flat for the third quarter.1 Though strong corporate earnings early in the period and promising trade talks buoyed sentiment, US trade rhetoric and economic turmoil in Turkey weighed on investor outlooks for the region. Uncertainty surrounding Britain’s exit from the European Union and the Italian government’s budget plans also sparked apprehension at times. Europe’s revised second-quarter GDP figures showed growth of 2.1% year-on-year in the euro area.

Asian equities collectively finished the quarter nearly flat, weighed down by Chinese markets.1 The China-US trade dispute continued to dominate sentiment. In July, China announced measures intended to stimulate domestic consumption amid the intensifying trade skirmish. China’s second-quarter 2018 GDP rose 6.7% year-on-year, in line with consensus expectations.4 Elsewhere in Asia, Japan’s second-quarter GDP rose 0.7% quarter-on-quarter, beating consensus expectations.5 India’s GDP growth for the April–June quarter exceeded consensus expectations at 8.2% year-on-year, the strongest growth rate since 2016.6 China’s announcement of stimulus measures, which was taken as supporting exports from several Latin American countries, lifted some regional equities during the third quarter.

Looking Forward

Last quarter we discussed valuation and the “trade war.” This quarter we discuss the impact of rising interest rates, in relation to the economy and investments in general. This has particular relevance considering the way October has started with interest rates seeming to reach a tipping point effect on the stock market. In conclusion we have some thoughts on the US government deficit; we hope you enjoy the discussion.

In 1981, the yield on the 10-year U.S. Treasury bond peaked at 15.3 percent. For the next 35 years, investors enjoyed a relatively unbroken bull market in their bond portfolios. Interest rates slowly declined, and investors regularly gained positive annual returns on their bond investments. During this time, the income produced by these investments also slowly declined. In fact, interest on the 10-year U.S. Treasury bond fell below 1.5 percent in 2012 and again in 2016. Since this low, investors and advisors alike have watched the hawkish turn in U.S. monetary policy by our Federal Reserve result in rising rates globally.7

When market participants use the term “rising rates,” they’re typically referring to increases in the benchmark policy rate set by each country’s respective central bank. In the United States, the policy rate set by the Federal Reserve is known as the “fed funds” target rate. The fed funds target rate is the primary tool of the Federal Reserve to fulfill their dual mandate of sustaining employment and controlling inflation. Through the fed funds target rate, the Federal Reserve exerts control over short-term interest rates only. Rates on longer maturities are then determined by the markets.7

The level of interest rates has a profound impact on investments and the economy. Fundamentally, when the Federal Reserve lowers interest rates it reduces the cost to borrow money which encourages consumption. It stands to reason that raising interest rates tends to do the opposite; increasing the cost of borrowing money and discouraging consumption. Broader impacts include:

Currencies

If the interest rates in the US are higher than another country, this increases the demand for US Dollars. This happens because, if all things are equal, investors choose to hold the currency with the higher interest rates so they will earn more interest on their cash. This increase in demand can drive up the value of US Dollars when compared to a foreign currency. It can also lead to higher demand for other domestic assets such as real estate, or stocks.

Company Earnings Related to Currencies

The increase in interest rates over the past year has contributed to an increase in the US Dollar verses many other currencies. This currency change results in earnings which were created overseas in foreign currencies being reduced when they are converted back to US Dollars. For example, if the price of an iPhone is 1,000 Euros, and the exchange rate of Euros to US dollars is 1.15, then the sales price is 1,150 in US dollars. But if the exchange rate changes to 1.10, then the sales price would now be $1,100 in US dollars. So the sales price, and therefore the company revenue per iPhone, went down without a change in the sales price denominated in the local currency.

Conversely, purchases of goods and commodities made overseas with these US dollars which have increased in value relative to foreign currencies can buy more goods and commodities than they used to. This can reduce inflation in the United States. Increasing tariffs on these goods and commodities coming into the US reduces this benefit.

Company Earnings Related to Debt

When interest rates increase companies who need to refinance debt may have to pay a higher interest rate on the new debt. Debt at higher interest rates can reduce earnings.

Company Earnings Due to Sales

If consumers are paying higher interest rates, the increased interest cost will impact them through credit card debt and when they borrow money to purchase a home or an automobile. This increase in cost may discourage, delay, or reduce the amount of a purchase. This reduction in sales can easily be seen to impact the earnings of an automobile company. If the automobile company makes fewer cars, employing fewer people, there can also be additional impacts. For example, if there are fewer employees making cars, the buinesses who provide goods and services to those former employees are impacted. It is also possible that due to growth and inflation in other parts of the economy, buyers can pay the higher prices and there is not a reduction in employees at the automobile companies.

Often stocks in various industries can provide a hint of what is actually going on as investors make buy or sell decisions based on their view of future earnings. For example, as we write this letter the stocks of two home builders and two automobile manufacturers have been under pressure. Toll Brothers and KB Homes are down approximately 45% and 51% from their highs earlier this year.8 Ford and General Motors are down approximately 37% and 31% from their highs earlier this year.8 These are companies whose sales and profitability is impacted by increased interest rates.

This impact is what Chris Rupkey, chief financial economist at MUFG is referring to in the following quote about US economic growth. “Interest rates are starting to bite a little…” “We’re not going to get 3% sustainable growth if consumers don’t buy cars and homes.”

Supply and Demand of Investments

Every investor has a choice of what to put their money in. While stocks have historically provided attractive long-term returns, bonds can provide greater stability and a fixed income. To use an extreme example, when bonds are paying 1%, there is a greater incentive to endure the ups and downs of owning stocks. When bonds are paying 8%, there is less incentive to endure the volatility of owning stocks. While this is simplistic, and there are many other factors to consider when making investment decisions, the concept is important. Demand for all other investments is related to the interest rates investors can receive by holding bonds. Especially the interest rates they can receive by holding bonds they feel have very little repayment risk, such as US Treasury Bonds.

Bond Values

As stated earlier, the reserve banks set short-term interest rates and influence to a lesser degree long-term rates. The long-term rates are set by the supply and demand forces at work in the markets. The value of bonds held by investors is reduced when these long term market interest rates rise. For example, if you own a bond issued by Disney paying 3% for the next 20 years, and the next day Disney issues bonds which will pay 6% for the next 20 years, then the new bond is more desirable than the bond you own. To entice someone to buy your bond which pays 3% instead of the new bond which pays 6% you must lower the price of your bond. In the end, it will still be expected to mature in 20 years, but you will have earned 3% a year while those who waited earn more. The opposite is also true. If you own a bond paying 3%, and the next day Disney issues a bond paying 1%, investors would rather own your bond. Therefore your bond is worth more than the new bonds.

Due to this situation and the low current interest rates, we have invested 1/3 of our bond portfolio in floating rate bonds which adjust their interest rate quarterly, 1/3 in bonds due in 1-3 years, and 1/3 in global bonds due in 1-5 years. We are earning less interest than if we invested in longer-term bonds, but we are avoiding a great deal of the potential risk associated with rising interest rates.

Current Stock Values

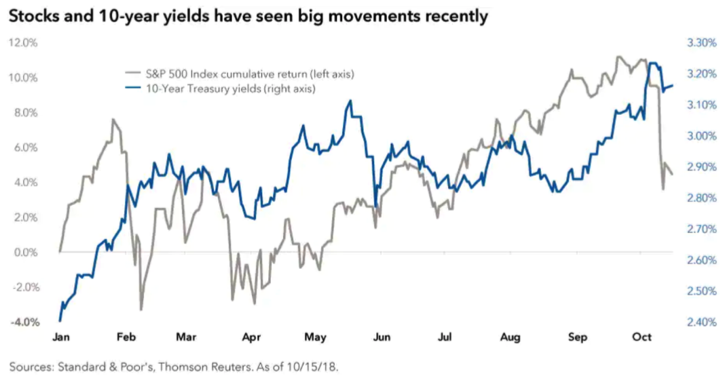

As seen in the following chart interest rates during October have upended the stock market. Capital Group economist Darrell Spence provides the following color commentary. “Equity valuations were elevated, and the market had been underestimating what the Federal Reserve said it was going to do regarding increasing short-term rates. “The stock market pullback is not particularly surprising when you consider that rates are rising, the labor market is tight, and the Federal Reserve is removing some liquidity from the system,” And there is a trade dispute with China that could put further pressure on the economy.”

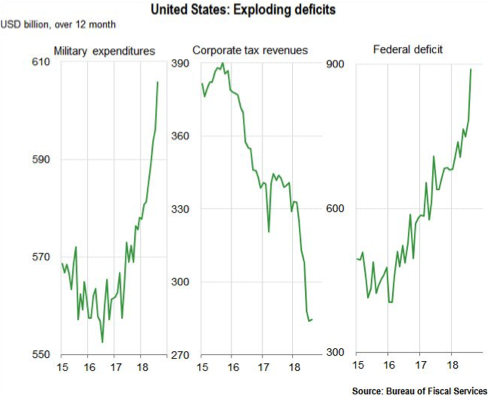

Deficit Spending

The exploding government spending and reduction in tax revenue in the United States concerns us. We can grow our way out of this, but a recession could make things look worse. Ideally, deficits are reduced during economic expansions and can be increased during economic recessions to stimulate growth, but neither side of the political aisle seems to be willing to make this politically unpopular choice to reduce spending or save money. This is happening while the two largest buyers of government debt are reducing their holdings, the US Federal Reserve and China.

In summary, interest rates obviously impact investment decisions. In particular, higher stock market valuations become harder to justify as interest rates increase. Even though the US economy continues to show strength, rising rates, rising oil prices, and a tight labor market could create margin pressure as well as revenue challenges. If the current pullback continues, it may create more favorable entry points. We might be wrong, but considering the sum of the evidence we believe it is prudent to continue to exercise caution.

If you have thoughts or questions about any of the information we’ve shared or on any other subject, please don’t hesitate to call us. We are grateful you allow us to serve you and your family and we will continue to make every effort to earn the trust you’ve bestowed on us.

Sincerely, Your CCA Investment Team

Advisory services offered through Cravens & Company Advisors, LLC, an SEC Registered Investment Advisory Company. Securities offered through, and advisory services may also be offered through, FSC Securities Corporation, an Independent Registered Broker/Dealer. Member FINRA/SIPC and a Registered Investment Advisor. Not affiliated with Cravens & Company Advisors, LLC.

Investing involves risk including the potential loss of principal. Investing involves risk including the potential loss of principal. International investing involves additional risks including risks associated with foreign currency, limited liquidity, government regulation, and the possibility of substantial volatility due to adverse political, economic and other developments. The two main risks associated with fixed income investing are interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risks refer to the possibility that the issuer of the bond will not be able to make principal and interest payments. Investments in commodities may entail significant risks and can be significantly affected by events such as variations in the commodities markets, weather, disease, embargoes, international, political, and economic developments, the success of exploration projects, tax, and other government regulations, as well as other factors. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance is no guarantee of future results. Please note that individual situations can vary. Therefore, the information presented here should only be relied upon when coordinated with individual professional advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of FSC Securities Corporation. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product.

1.Source: © 2018 Morningstar, MSCI.

2.Source: US Bureau of Labor Statistics.

3.Source: US Bureau of Economic Analysis.

4.Source: National Bureau of Statistics of China.

5.Source: Statistics Bureau of Japan.

6.Source: Ministry of Statistics and Programme Implementation, Government of India.

7.Source: Positioning Portfolios for a Rising Rate Environment by Elizabeth K. Miller & Andrew N. King, Trust and Estates Journal September 2018

8.Source: Schwab Advisor Services as of October 23, 2018