1st Quarter 2017

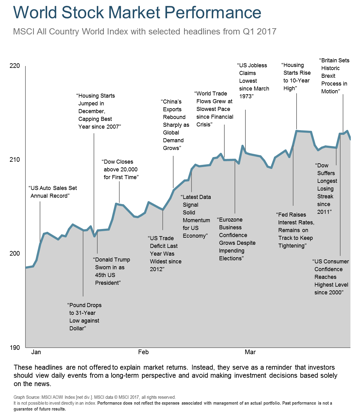

Global equity markets rose in the first three months of 2017, providing stocks with their strongest first quarter performance since 2012. Equities were buoyed by broadly positive economic indicators from the United States, Europe, China, and Japan. Optimism about US President Donald Trump’s policy initiatives and concerns about upcoming elections in Europe were prominent early in the quarter, though investor sentiment on politics became less of a factor by period-end. Growing skepticism surrounding the timing and the extent of the Trump administration’s ability to enact a pro-business agenda—exacerbated by struggles to pass a healthcare bill to replace the Affordable Care Act— weighed on sectors that had previously benefited from the “Trump trade,” namely financials and industrials. Meanwhile, signals from the Trump administration in March regarding trade indicated some potential moderation from its earlier protectionist stance, and this shift generally supported the markets of US trade partners. In Europe, support for populist candidates appeared to slip in March, which comforted markets. Regionally, Latin American, Asian and European stock markets outperformed the global index. Conversely, US stock markets rose but trailed the global index[1].

The US Federal Reserve increased its key short-term interest rate by 25 basis points (to a range of 0.75% to 1.00%) in mid-March, signaling its continued confidence in the improving economy. Fed Chair Janet Yellen offered a broadly positive assessment in March. US economic data generally has unfolded to the upside, reflecting gradually accelerating inflation, improved manufacturing activity, stronger housing demand and stable consumer spending.

European equity markets mostly rose in the first quarter, supported by largely positive economic data. Markets experienced some volatility, primarily due to concerns about upcoming elections in the region and Britain’s preparations to leave the European Union (EU). However, by quarter-end, investor concerns lessened. A televised French presidential debate eased investor concerns that nationalist candidate Marine Le Pen would win that country’s presidency or that her party would make significant gains in parliament. At quarter-end, British Prime Minister Theresa May formally triggered Article 50 to begin the country’s negotiations on exiting the EU. Asian equity markets overall rose in the first quarter, substantially outpacing global stocks as a group. China’s manufacturing sector surprised in March with the fastest growth pace in five years[2].

Looking Forward

Through the past 20 years or so we have witnessed many market events and seen how those events influence the feelings of our clients and other investors. Human nature is a powerful thing, and no one is immune from its influence. Multiple times we have seen investors very concerned over losing money, and we are currently at the opposite end of that spectrum. Regretfully it’s normal for investors to be scared when valuations are cheap and confident when valuations are high. This shift in views has been a long time in coming from the lows of 2009. This shift doesn’t mean returns from this point will necessarily be bad. But it does indicate the risk level in stocks right now is higher than it used to be. Elevated risk doesn’t just show up in our gauges of Investor Psychology, but is also reflected in Monetary Policy and Valuation gauges, while our Market Trend gauge is still positive.

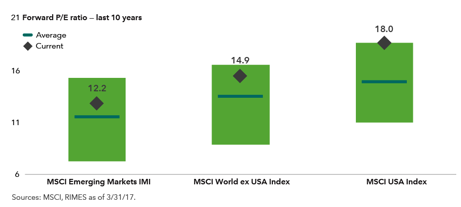

We would also note the high valuation is mostly in the US market which has been the strongest market the last three years. There are many ways for the discrepancy between the valuation of international markets to be adjusted, and not all involve the US market declining. The international markets could just increase more, or the earnings from companies based in the US could have a large increase. We don’t pretend to know how this unfolds, but we do believe the risk in US stocks is currently higher than the risk in international stocks due to current valuations. PE ratio may be a hard concept to understand in comparison. The same numbers below can also be illustrated as an Earnings Yield, so PE ratios of 12.2, 14.9, and 18 convert to Earnings Yields of 8.2%, 6.7%, and 5.6%[3]. The Earnings Yield can be viewed as the percent return if stock values didn’t fluctuate and all the earnings were distributed to investors. We believe investments dollars will eventually flow to where they are most rewarded.

What do we do with this view? It presently makes us more cautious in most of our strategies. Market Capture remains fully invested as always to “capture” whatever return markets provide. In Risk Managed we have adjusted risk by reducing some of our normal allocation toward US stocks. Our more focused portfolios are holding more cash than normal and our Fixed Income strategy has shifted toward more conservative bonds. These are not radical adjustments, but shifts based on the current market environment.

Announcement

As many of you know, Cravens & Company Wealth Management is affiliated with Progressive Savings Bank. It is with a heavy heart that we deliver this news. Steve Rains, the President of Progressive Savings Bank passed away on Monday, April 17, 2017. He was a man of great compassion and a fervent leader. He graciously served his community delivering exceptional financial services. The passion he had for his employees and customers was unsurpassed. Steve’s philanthropic efforts were and will continue to be impactful. He championed the legacy of his father and his mother through his efforts with the Rains Foundation, a non-profit charity that awards scholarships for higher education. Steve was also a previous chairman of the Tennessee Technological Foundation board, another non-profit organization that provides support for Tennessee Technological University.

During this tragic time, we find strength and confidence in this great organization that Steve and his father Lyndon worked so hard to build. This event, while heartbreaking, has caused our organization to unite in a strong way. We will continue to deliver exceptional financial services to our clients. We find hope in the future and will do our utmost to continue this incredibly strong legacy that has permeated the hearts and minds of not only many of our clients and employees but also many others.

If you have thoughts or questions about any of the information we’ve shared or on any other subject, please don’t hesitate to call us. We are grateful you allow us to serve you and your family and we will continue to make every effort to earn the trust you’ve bestowed on us.

Sincerely,

Your CCA Investment Team

Cravens & Company Advisors, LLC is a wholly-owned subsidiary of Progressive Savings Bank. Investing involves risk including the potential loss of principal. Investing involves risk including the potential loss of principal. International investing involves additional risks including risks associated to foreign currency, limited liquidity, government regulation, and the possibility of substantial volatility due to adverse political, economic and other developments. The two main risks associated with fixed income investing are interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risks refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. Investments in commodities may entail significant risks and can be significantly affected by events such as variations in the commodities markets, weather, disease, embargoes, international, political, and economic developments, the success of exploration projects, tax and other government regulations, as well as other factors. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance is no guarantee of future results. Please note that individual situations can vary. Therefore, the information presented here should only be relied upon when coordinated with individual professional advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of FSC Securities Corporation. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product.

[1] Source: © 2017 Morningstar, MSCI.

[2] Source: People’s Bank of China.

[3] Source: FactSet Research Systems, Inc.