With COVID-19 dominating almost every aspect of the news, we won't spend time trying to offer more. Suffice it to say, we are living in a historical moment that few of us, if any, have witnessed before. The actions taken by our federal, state, and local governments are akin to wartime measures. While they may feel extreme, the spread of the virus and its potential impact on our health and economy, warrant extreme measures. Hopefully, with our cooperation, they will improve the outcome.

Pandemics are extremely rare, but bear markets are not. Epidemiologists tell us we are looking at a once in a century event, the last occurring in 1918. While bear markets are reasonably common, we haven't seen one for the past decade. Historically, we've experienced a market decline of 20% or greater on average every ten years. Examples include 1929, 1946, 1961, 1968, 1973, 1980, 1987, 2000, and 2007. While the speed of this decline has set records and been painful thus far, the reset itself is not unexpected nor uncommon.

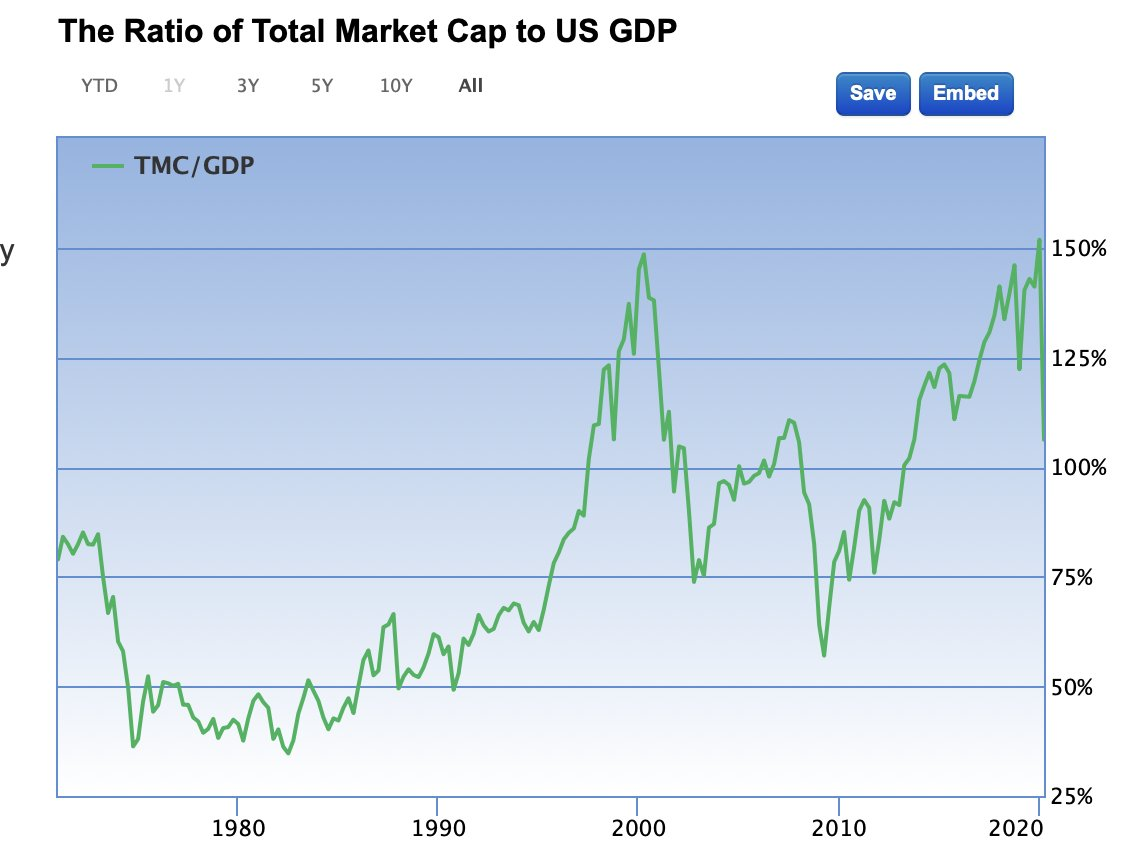

Since the onset of the crisis, stock valuations have improved significantly. The chart below details the relationship between the value of the U.S. equity market and the country's total economic output (GDP). The drop, from a record 158% in February to Friday's reading of 106%, was swift. Given the severity of the situation and elevated starting point, we may see further price declines and valuation improvements. We all appreciate the logic of buying low and selling high. Unfortunately, our emotions often hinder us from acting on the rationale that improved valuations have increased expected future returns for investors who buy stocks today.

Ratio of Total Market Capitalization to Gross Domestic Product

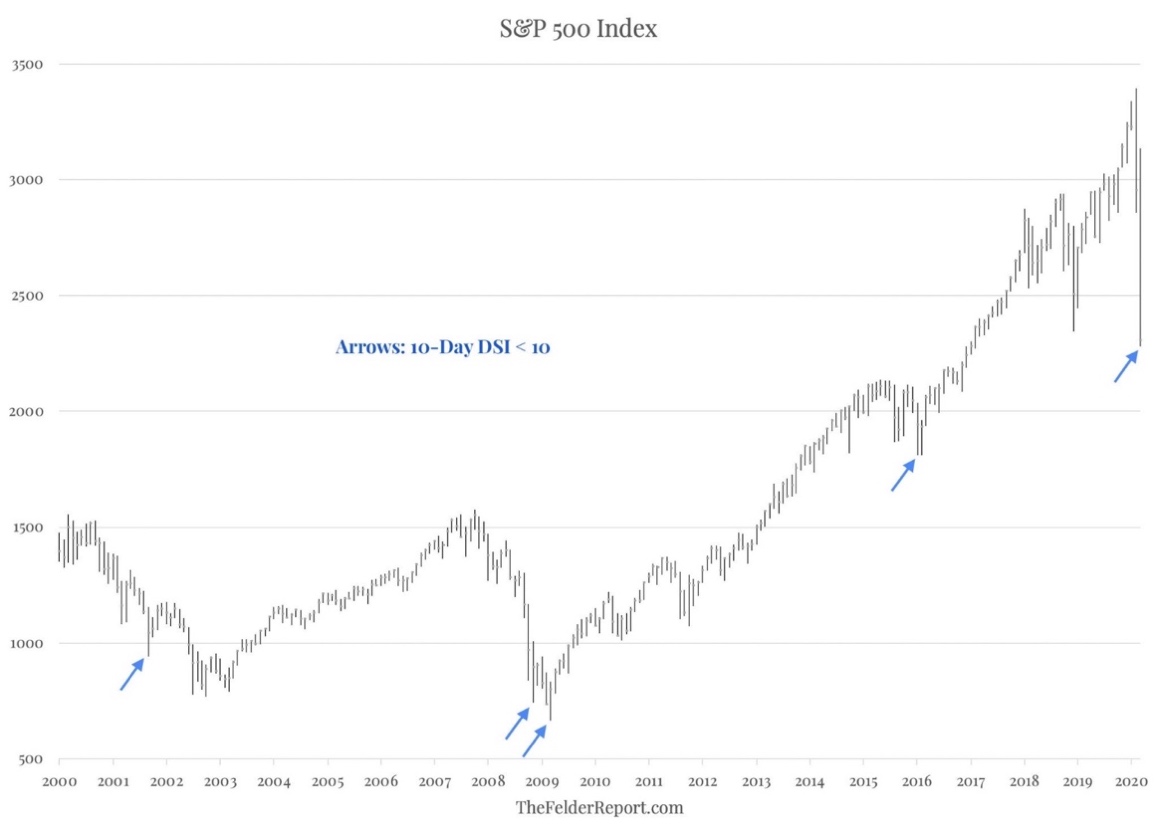

By almost all measures, the market is presently oversold. Many, but not all, investment volatility and psychology indicators have reached points that have historically led to at least short-term increases. An example is the 10-Day average of the Daily Sentiment Index, a measure of small investor behavior, and the 5th time it has been this low over the past 30 years.

Daily Sentiment Index

Investment Implications

The stock market is the only market in the world where decreases in price discourage buying. Stock valuations have declined to levels that have been historically attractive investment opportunities, but there are logical reasons for a further decline in this situation. We have held off on buying but will likely soon start implementing the Phasing Plan we outlined last week.

We continue to expect COVID-19 will be a transitory event, with life returning to a version of normal in the future. Just like how life changed after 9/11, there may be long-term changes after this disaster. Air travel may look different, but we expect people will still choose to fly from Tennessee to California instead of drive. We anticipate the news will get worse before it gets better but is watching for the point when investors look past the moment and to the ultimate resolution of all the current crisis.

Portfolio changes this week were as follows:

- 3/17/2020 Sold Short Term US Treasury Bond ETF

-

3/17/2020 Bought Short Term US Mortgage Bond ETF

- The gap between Treasury Bonds and Mortgage Bonds widened. This means we receive higher interest rates by making this change, while still retaining AAA-rated government-backed bonds.

- 3/18/2020 Sold Corporate Money Market Fund

-

3/15/2020 Bought US Government Money Market Fund

- Money market funds are expected to always trade at a $1 value per share. Due to the 2008 financial crisis, the US government made a change in how they operate. While we do not expect such a scenario, the change leaves open the possibility that a fund could lose value. We don't want to ignore this risk due to the current environment.

-

3/18/2020 Sold Kroger's (Quality Focus)

- The gain in Kroger's shares has exceeded our short-term expectations since purchase in July of 2019. While the news is all positive for the company, we concluded to sell a stock that has increased during the decline and purchase a company with greater potential long-term growth.

Looking Forward

Watching account values decline is stressful. Hopefully, the extra cash we are holding reduces the pain, but if that were the only advantage it provided, then it would be an insufficient balm. The real value of cash in a portfolio is it creates the opportunity to make attractive investments when markets inevitably decline. Markets in total are down around 30%, but many companies are down over 50%. The opportunity has quickly arrived; we will now do our best to make reasonable investments in light of the potential risk and reward with the cash in your portfolios.

We delayed beginning purchases last week due to the market's continued decline in the face of fiscal spending commitments by the governments of the world and monetary commitments by the central banks of the world. This was the "good news" investors were waiting on, yet COVID-19 concerns overwhelmed the news. We took this as a sign to be cautious for the moment. Moving forward, we anticipate our investments to be measured and in keeping with the phases we laid out previously. Of course, this is a fluid environment, and we plan to weigh all the information available in the decision process.

The global stimulus is hard to comprehend, measured in trillions of dollars (1 trillion seconds is 31,709 years). This is not money that has been set aside for a rainy day; it must be borrowed. This significant amount of debt may be the catalyst to create a shift toward inflation at a time when most investors had given up on ever seeing it again. But that's the way investing works, once everyone is on one side of the boat, the odds of them getting wet increases. We will be watching for this and working on how to position your investments to deal with this change if it evolves.

Summary

We hope the details we are sharing provides some confidence in and understanding of our reasoning in planning. COVID-19 is a serious crisis, but it will pass. Until then, we must avoid the mindset of selling and waiting until everything improves – that’s often a recipe for selling at lows, buying at bear rally peaks, and compounding the damage. There will be a vaccine, and there will also be stories of heroism and courage. Banks are in better shape than they were in 2008, and there’s a lot of amazing ingenuity, creativity, and intangible value underlying the US economy. We will one day look back on this time as being an incredible affirmation of the human spirit and the American ideal. The main thing now is to follow the guidelines that have been laid out, keep our distance, and stay safe.

If you have thoughts or questions about any of the information we've shared, or on any other subject, please don't hesitate to call us. We are grateful you allow us to serve you and your family, and we will continue to make every effort to justify the trust you've bestowed on us.

Sincerely,

Your CCA Investment Team

Advisory services offered through Cravens & Company Advisors, LLC, an SEC Registered Investment Advisory Company. Securities offered through and advisory services may also be offered through, FSC Securities Corporation, an Independent Registered Broker/Dealer. Member FINRA/SIPC. Not affiliated with Cravens & Company Advisors, LLC.

Investing involves risk including the potential loss of principal. Investing involves risk including the potential loss of principal. International investing involves additional risks including risks associated with foreign currency, limited liquidity, government regulation, and the possibility of substantial volatility due to adverse political, economic and other developments. The two main risks associated with fixed income investing are interest rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risks refer to the possibility that the issuer of the bond will not be able to make principal and interest payments. Investments in commodities may entail significant risks and can be significantly affected by events such as variations in the commodities markets, weather, disease, embargoes, international, political, and economic developments, the success of exploration projects, tax, and other government regulations, as well as other factors. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance is no guarantee of future results. Please note that individual situations can vary. Therefore, the information presented here should only be relied upon when coordinated with individual professional advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of FSC Securities Corporation. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product.